Listen to this article >

Listen to this article >

Modern business survival is dependent on perpetual innovation. At perhaps no point is this more evident than in times of significant economic and societal unrest, as we are in today. In the years to come, we will inevitably look back at 2020 as a year of major transitions.

Among the changes is the rapid acceleration of the digital transformation that has been taking place for several decades. In the past couple of years, a new class of industry giants has emerged and become public companies, built upon the technology wave that led the transition to mobile and cloud. From the recent successful IPOs of Snowflake, Unity, and Sumo Logic – and last year’s IPOs of Uber, Lyft, and Pinterest among many others – it is evident that we are now living in a new era of cloud technology.

Strong public market debuts in the midst of the economic chaos that has defined 2020 demonstrates a collective maturation – and expansion – of the cloud and developer infrastructure ecosystem. Moreover, their success shows that Wall Street and public market investors are recognizing the true value of tech and SaaS business models, underscoring that the new moats of business defensibility is inherently scalable even at the worst of times.

The rate of innovation at these cloud-first companies has quickly eclipsed that of their predecessors. I predict the next few years will be a period of significant growth in the cloud-first ecosystem, based on the way technology has advanced over the past few decades. From personal computers in the 1990s into the dot.com of the early 2000s, followed by the mid-2000s ascent of mobile and cloud, each era is defined by the core technology shifts that made it possible for businesses to advance through changing market conditions. Importantly, each major technological leap forward was achieved by evolving from the foundational toolset built by the previous generation.

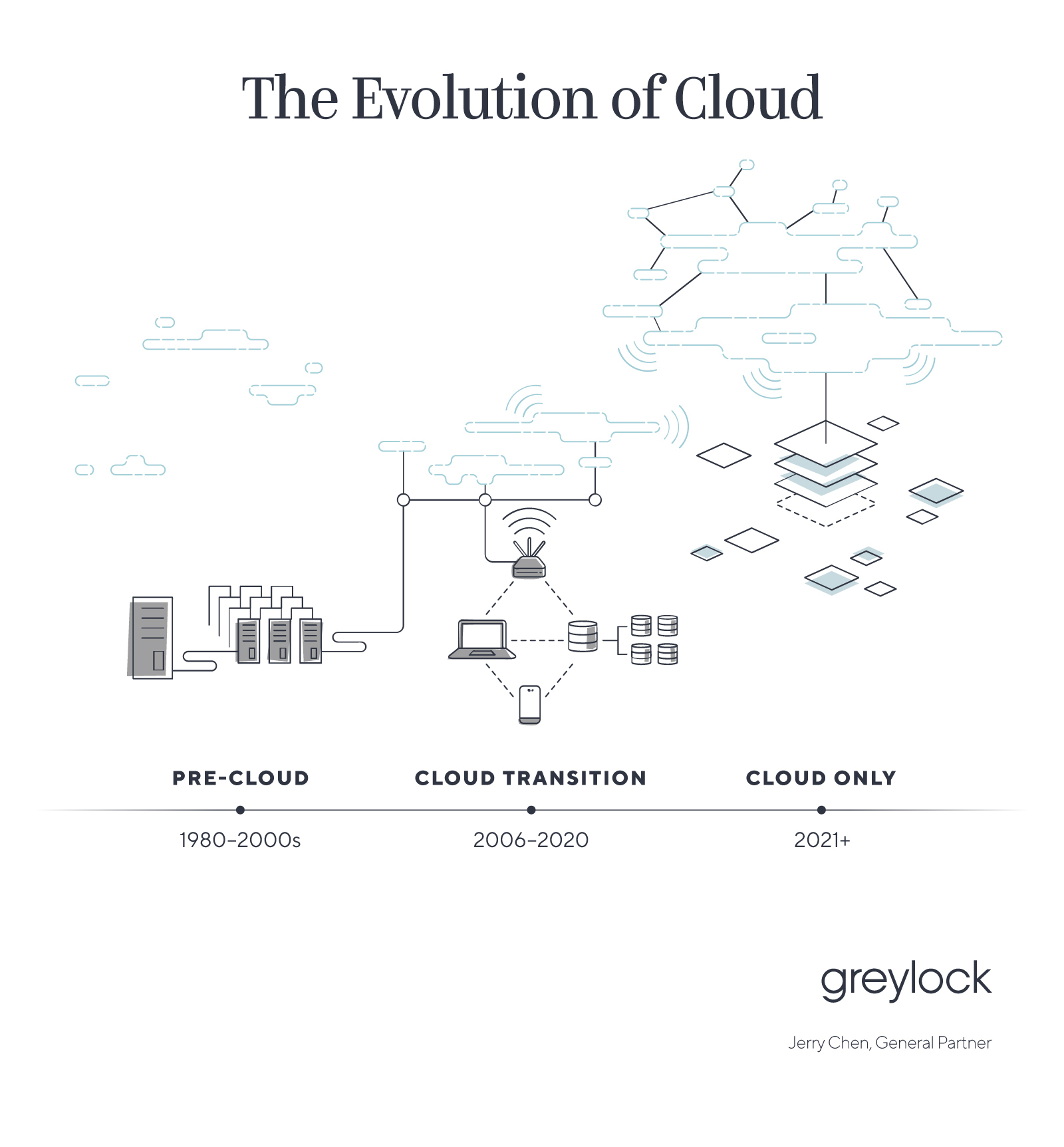

PRE-CLOUD

(Era 1980s – mid 2000s)

In the 1980s and 1990s, “dinosaur” legacy companies like DEC, Sun Microsystems, HP, and IBM roamed and ruled the earth. Other pre-cloud “prehistoric” giants like Oracle and SAP existed, and – similar to the whales and turtles still on earth today – managed to evolve and maintain a significant presence as the dinosaurs became extinct. Oracle and SAP had each created moats as the system of record for large enterprises. Both their installed base of customers, strong distribution channels, and ecosystem of applications around them to transition into the cloud era, maintaining their relevance to this day. Meanwhile, there were also several internet native companies like Netscape, Yahoo, and AOL that were born – and then more or less faded from relevance – during the same era. Dell Technologies is an example of Darwin’s axiom that the most ‘adaptable’ survive as it evolved from PCs and servers. Via acquisitions and investments in companies like VMware, the company was able to incorporate the necessary survival skills that have kept it relevant to this day.

Yet, although several legacy giants have managed to stay relevant, the default enterprise stack is no longer on premise hardware and licensed software. It has shifted permanently to mobile and cloud. In the past four years, the new generation of leaders have emerged around the “Big Cloud” ecosystem of Amazon Web Services, Google Cloud Platform, and Microsoft Azure.

CLOUD TRANSITION

(Era 2006-2020)

The debut of Amazon Web Services in 2006 and the launch of the iPhone in 2007 mark the beginning of the cloud and mobile platform transition. The next stage of competitive product development and new company formation was swift: Amazon’s success was soon followed by Microsoft Azure and Google Cloud Platform, forming the “Big 3” of cloud. For the next decade and a half, companies moved their products to cloud or mobile. Microsoft Exchange and Office were succeeded by GMail and Google Apps before Microsoft could respond with Office 365. During this transition, new collaboration and productivity companies like Dropbox, Slack, and Notion were born. Cisco Webex was replaced by the cloud-based offering of Zoom. Video and photo sharing went from a primarily desktop experience to a mobile first app.

During this transition era to the cloud, founders and companies tried to cater multiple environments: on-premise private clouds, big cloud platforms, and hybrid cloud environments. Additionally, the twin evolution of mobile and cloud technology birthed an entirely new generation of apps like Instagram, TikTok, Uber and DoorDash that previously would not have been possible. In parallel, the underlying computing infrastructure stack was disrupted by the cloud – both by the new consumption-based business model that put developers into the role of king-maker, as well as the need to create elastic infrastructure stacks that could support cloud and mobile applications. New technologies like Docker and Kubernetes become the new compute layer, while new databases like Hadoop, MongoDB, and Elastic were open sourced to make sense of the tsunami of data generated by these new applications.

CLOUD ONLY

(Era 2021 and beyond)

While the past fifteen years of the cloud transition has produced some large and likely enduring companies, today we are seeing new companies that are not part of the cloud transition or a hybrid cloud generation. They aren’t even cloud-first– they are cloud only. What does this mean? Founders and companies built for cloud only are not trying to serve legacy and cloud environments. They are cloud native and cloud only. They are built and architected from the first lines of code to take advantage of cloud compute, storage, and networking, in the same way that software written in the 1990s was assumed to be running on Windows or Solaris. Like the app-based companies that would never have been conceived without the smartphone, the entire architecture of this new breed of cloud-only companies assumes certain capabilities in order to exist. Likewise, as the cloud transition opened up new opportunities for businesses and business models, the success of those companies has created another avenue for innovation. GSuite, Microsoft Office and the like are working alongside cloud-only productivity and collaboration tools from companies like Asana, Figma and Coda. Founded during the height of the cloud transition, these latter companies understood where the market was headed, and thus built for the cloud-only future.

Why does being only on the cloud matter? Software from cloud-only companies possess a subtle – but important – distinction from software that was formed during the cloud transition. Hybrid infrastructure stacks built during the transition were developed to run on-premise in a static environment, and then ported over to run on the cloud. Essentially, they treated cloud compute, storage, and networking like on-premise stacks operated by a third party. Conversely, software written for cloud-only assumes logical disaggregation of compute, storage, and networking, meaning it can take advantage of the intrinsic elasticity of the cloud. This is why simply moving an open source database or project like Elastic or Kafka to the cloud doesn’t make it a cloud-only service. MongoDB realized this and launched Mongo Atlas, which began with the open source MongoDB project and was further augmented by significant code to make it a true cloud offering. Likewise, Snowflake separated storage from computing, creating a truly cloud-only program that led to better workflows for developers. Other pioneering companies are using cloud and building new moats such as serverless infrastructures, which pushes data, compute functions, and apps to the edge.

Now, there is a cadre of startups that were founded specifically to meet the expanded needs of the cloud generation. Led by founders who worked at iconic tech companies that rose to the top during the cloud transition, these companies recognized the need for more powerful tools for observability, data, analytics and security. Cloud-only companies including Rockset, Chronosphere and Cato Networks are quickly becoming indispensable partners to organizations across multiple industries including ecommerce, finance and supply chain logistics. Rockset, which recently closed on its series B, identified a problem associated with the shift to mobile cloud-based technologies: a huge increase in data, from which existing analytics tools could not quickly or easily derive insights. Rockset’s founders, armed with experience with web-scale data management and distributed systems, understood the changing nature of data applications and created a serverless, real-time indexing database that delivers analytics at a speed and scale previously not possible. Likewise, Cato Networks, which recently closed a series E and is valued at more than $1B, identified a gap in the expanding cloud landscape to the edge and created the first Secure Access Service Edge (SASE) Platform.

The early traction of these cloud-only startups is also a call to action: What needs to be built to fuel the next generation?

- First, in a world where Big Cloud dominates the landscape, a startup must own a problem space and then own the solution awareness to that problem. In a cloud only world, your competition is not only just a click away but an API call away.

- Second, cloud-only companies must leverage the underlying advantages of cloud architecture in terms of elasticity and scale.

- Finally, to be truly enduring, these next generation of companies must build their own moats beyond the walls of the big cloud vendors. This could be extending their reach to the edge or home or building a deep IP moat around themselves.

As we near the end of 2020, we look to the next year and beyond as a time of rapid technological and business model evolution, far outpacing the rates of decades past. We’re at the next edge of possibility at a time when innovation is more than the thrill of advancement – it is an acute need.